The IRS has released a new round of guidance (IR-2025-117 and Notice 2025-68, both issued December 2, 2025) clarifying how a new type of retirement account, called a Trump Account, will work when it becomes available in 2026.

What is a Trump Account?

A Trump Account is a new type of tax-advantaged individual retirement account (IRA) designed for children under age 18, created by the One Big Beautiful Bill Act (OBBBA) and now governed by Section 530A of the Internal Revenue Code.

At its core, a Trump Account is intended to help families begin long-term investing for a child well before adulthood. Unlike traditional or Roth IRAs, Trump Accounts do not require the child to have earned income. Instead, parents and other permitted contributors may fund the account on the child’s behalf.

The IRS has confirmed that contributions cannot begin until July 4, 2026, and many administrative details are still being finalized.

Who is Eligible?

A Trump Account may be established for an individual with a social security number who has not turned 18 before the end of the calendar year in which the election to open the account is made. The election is expected to be made by a parent, legal guardian, adult sibling, or grandparent using Form 4547, Trump Account Elections(s). This form can be filed with the parent’s tax return, separately with the IRS, or completed online at trumpaccounts.gov. There are stricter rules about who can file the election if requesting pilot programs contributions. Only an individual who expects the child will be his or her qualifying child for tax purposes can file the election to include contributions.

Although the IRS has not yet published full custodial rules, Trump Accounts are expected to operate similarly to custodial IRAs, with an adult acting as trustee or custodian until the child is legally permitted to control the account.

How do Trump Accounts work?

Contributions

Under current guidance, total contributions to a Trump Account are generally capped at $5,000 per year, aggregated across all sources. This limit applies regardless of whether contributions come from parents, relatives, employers, or other eligible contributors. Exceptions to the $5,000 cap include the $1,000 pilot program contribution (discussed below) and qualified general contributions from governments or charities, such as the recent $6.25 billion pledge from Michael and Susan Dell. Beginning after 2027, this annual limit will be indexed for inflation.

Employers may contribute up to $2,500 per year to a Trump Account for an employee’s child through an employer Trump Account contribution program. These contributions are excluded from the employee’s taxable income, but they do count toward the $5,000 annual limit. Employers can also offer contributions to a dependent’s Trump Account through a salary reduction arrangement under a Section 125 cafeteria plan, which would allow employees to redirect salary on a pre-tax basis into the account.

Investments

Funds held in a Trump Account must be invested in broad-based U.S. equity index funds, such as mutual funds or exchange-traded funds that track the S&P 500 or another index primarily composed of American companies. Individual stocks, cryptocurrencies, and alternative investments are not permitted under current rules. Additionally, eligible funds have annual fees and expenses that do not exceed .1%.

Withdrawals and Tax Treatment

Trump Accounts are subject to strict withdrawal limitations. No distributions may be taken before January 1 of the year in which the child turns 18. There are very few exceptions for withdrawals. Funds may be rolled over to another Trump account or an ABLE account for the same beneficiary, to remove excess contributions or upon death of the beneficiary. Notably, hardship is not an exception to allow withdrawal.

After the child reaches the age threshold of 18, the account is generally treated as a traditional IRA. Withdrawals are taxed as ordinary income, and early withdrawal penalties may apply if funds are accessed before age 59½, unless a qualifying exception applies. IRA basis rules also apply, which only tax the earnings and pre-tax contributions portion of withdrawals.

Pilot Program Contribution

Separate from regular contributions, the federal government will make a one-time $1,000 pilot contribution to certain Trump Accounts. This feature has received much attention, but it applies only to a limited group of children.

To qualify, the child must be:

- A U.S. citizen, and

- Born between January 1, 2025, and December 31, 2028, and

- Properly enrolled through a timely Trump Account election completed by the qualifying child’s parent or legal guardian.

This $1,000 contribution does not count toward the annual $5,000 contribution limit. However, children born outside the 2025–2028 window will not receive this federal deposit unless Congress extends or modifies the program in the future.

Additional Available Funding

Michael and Susan Dell announced a $6.25 billion charitable commitment to add $250 to eligible children’s Trump Accounts. Children born before 2025 and 10 and under may qualify for this philanthropic seed money. In addition to the age requirement, children must have social security numbers and live in a zip code with a median annual income of $150,000 or less.

No separate application is needed. This philanthropic money is managed through the Trump Account infrastructure. Completing the election to open a Trump Account either on Form 4547 or online and requesting contributions should be sufficient to apply for the funds. Philanthropic funds are not guaranteed but the potential for “free money” makes the election worth it.

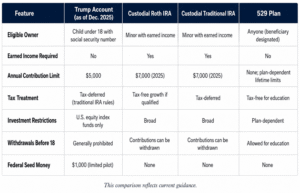

How Trump accounts compare to other common options

Many parents are already familiar with Roth IRAs, custodial Roth IRAs, and 529 plans, and may wonder how Trump Accounts fit alongside or compete with those tools.

This comparison reflects current guidance and highlights a key point: Trump Accounts are designed for long-term retirement-style savings, not education funding or short-term flexibility. In terms of retirement planning, they are a new option that allows for contributions even without earned income by the child.

What We Don’t Know Yet

Proposed regulations were issued March 2026 however uncertainties remain. The IRS has plans for additional regulations addressing:

- Contributions

- Distributions

- Reporting and coordination with IRA rules.

The IRS has explicitly requested public comments on several of these issues. signaling that additional guidance is expected however a timeline has not been announced.

What can parents do now?

Even though contributions cannot begin until July 2026, families can take steps now by familiarizing themselves with the rules, verifying eligibility for children born between 2025 and 2028 as well as before 2025. Consider speaking with a tax or financial advisor about how Trump Accounts may fit into their broader planning strategy.

Parents who already use 529 plans or custodial Roth IRAs should be especially cautious about assuming Trump Accounts are a replacement. At least for now, they appear to serve a distinct and more restrictive purpose.

A New Tool, Still Taking Shape

Trump Accounts are still very much a work in progress. The IRS’s December 2, 2025 notice as well as the proposed regulations, provide clarity on structure and intent while acknowledging further guidance is needed.

For families trying to make sense of these accounts, the key takeaway is this: Trump Accounts are real, they are coming, and they may be useful – but the full picture will not be clear until additional IRS guidance is released.

As with many new tax provisions, the details matter. Trump Accounts may offer a meaningful long-term savings opportunity for some families, but they are not a one-size-fits-all solution. Contribution limits, investment restrictions, tax treatment, and distribution limitations all play an important role in determining whether this new child-focused retirement savings account aligns with your family’s broader financial plan.

If you would like to discuss how a Trump Account may fit into your overall tax and investment strategy, our team at Maxwell Locke & Ritter is here to help. Contact us to evaluate your options and build a plan that supports your child’s future with confidence and clarity.