In software and recurring revenue transactions, valuation tends to revolve around ARR growth, retention metrics, and margin scalability. But as with any deal, the ultimate economics are not just determined by the headline multiple. They are also shaped by the definitions embedded in the purchase agreement, particularly indebtedness and net working capital (NWC).

In software deals, those definitions often carry even greater weight. Software companies’ balance sheets are structurally different: negative working capital is common, deferred revenue is significant, and traditional debt may be minimal. The delineation between NWC and indebtedness is less intuitive and far more negotiable.

While NWC mechanics remain important, it is the definition of NWC and indebtedness (particularly debt-like and off-balance sheet items) that often drives value transfer between buyer and seller.

Why Indebtedness Matters More in Software Transactions

Unlike asset-heavy businesses, software companies typically operate with limited traditional funded debt. As a result, indebtedness in software transactions becomes less about bank debt and more about other future economic obligations the buyer may be assuming at close.

For example, software companies typically carry significant deferred revenue balances and meaningful accrued expenses tied to growth (most notably commissions, bonuses, and other incentive compensation). In addition, buyers increasingly focus on “debt-like” obligations – items that may not be labeled as debt but nonetheless represent real future operating cash outflows.

Buy-Side vs. Sell-Side Tension

The tension between buyers and sellers is often amplified in software transactions given the nature of the balance sheet.

Buyers are underwriting cash conversion from ARR and anticipated future margin expansion and seek to capture any obligations that will consume future cash as indebtedness in the purchase agreement. Buyers want to be compensated dollar-for-dollar for taking on any future obligation eating into future cash flow.

Sellers, by contrast, are incentivized to emphasize the operational nature of liabilities on a software balance sheet (particularly deferred revenue and compensation accruals) and keep these items classified as NWC, while limiting indebtedness to clearly defined financing items. Sellers want to maximize transaction proceeds in the funds flow and limit what is classified as indebtedness.

The Real Focus: Debt-Like and Off-Balance Sheet Items

There is typically alignment around what constitutes traditional indebtedness: revolvers, term loans, convertible notes, and finance lease liabilities. The more consequential negotiations tend to center on debt-like and off-balance sheet items, where accounting presentation may diverge from economic substance.

Deferred revenue

Deferred revenue is often the most material point of contention. It is typically the largest liability on a software company’s balance sheet, yet its treatment in the transaction context varies from deal to deal. Buyers view deferred revenue as a performance obligation that requires real cash to service post-transaction, while sellers view it as a core feature of the recurring revenue model that is already reflected in ARR and appropriately captured in NWC.

The key nuance is that the cost to fulfill deferred revenue (e.g., hosting, support, and customer success) is usually a fraction of the recorded liability. As a result, a typical compromise acceptable to both buyers and sellers involves removing deferred revenue from the calculation of adjusted NWC and selectively treating the cost to service the balance as debt-like.

Employment-related liabilities

Sales commissions present a similar challenge. Under ASC 340, many software companies capitalize commissions, creating a disconnect between accounting treatment and cash deployment. Accrued commissions, particularly those tied to pre-close bookings, can be significant in high-growth environments. Buyers often view these as debt-like obligations, while sellers argue they are recurring operating expenses embedded in the business model.

Other areas of focus include accrued wages, bonus accruals, and earned-but-unpaid PTO. Although these items are typically reflected as current liabilities on the balance sheet (and thus classified in NWC), buyers are increasingly taking a “your-watch-our-watch” approach to employment-related liabilities and insisting they be classified as indebtedness. Although “your-watch-our-watch” sounds fair, this approach results in sellers paying for all pre-transaction accrued employment-related balances in the funds flow at close.

Future spend commitments

Future spend commitments (e.g., hosting commitments) have also become an area of increased scrutiny. Multi-year agreements with AWS or Azure, often with minimum spend thresholds, may not be fully reflected on the balance sheet. Buyers are increasingly focused on identifying above-market or underutilized commitments and assessing whether these represent economic obligations akin to debt.

Tax exposures

Software businesses often have uncollected and unremitted US sales tax exposure across jurisdictions. This exposure is often not accrued or under-accrued and can become a source of dispute if not clearly diligenced and addressed in the purchase agreement. Although these types of exposures may not be accrued on the balance sheet, a buyer will want to ensure it is adequately compensated for taking on the risk and remediating post-close.

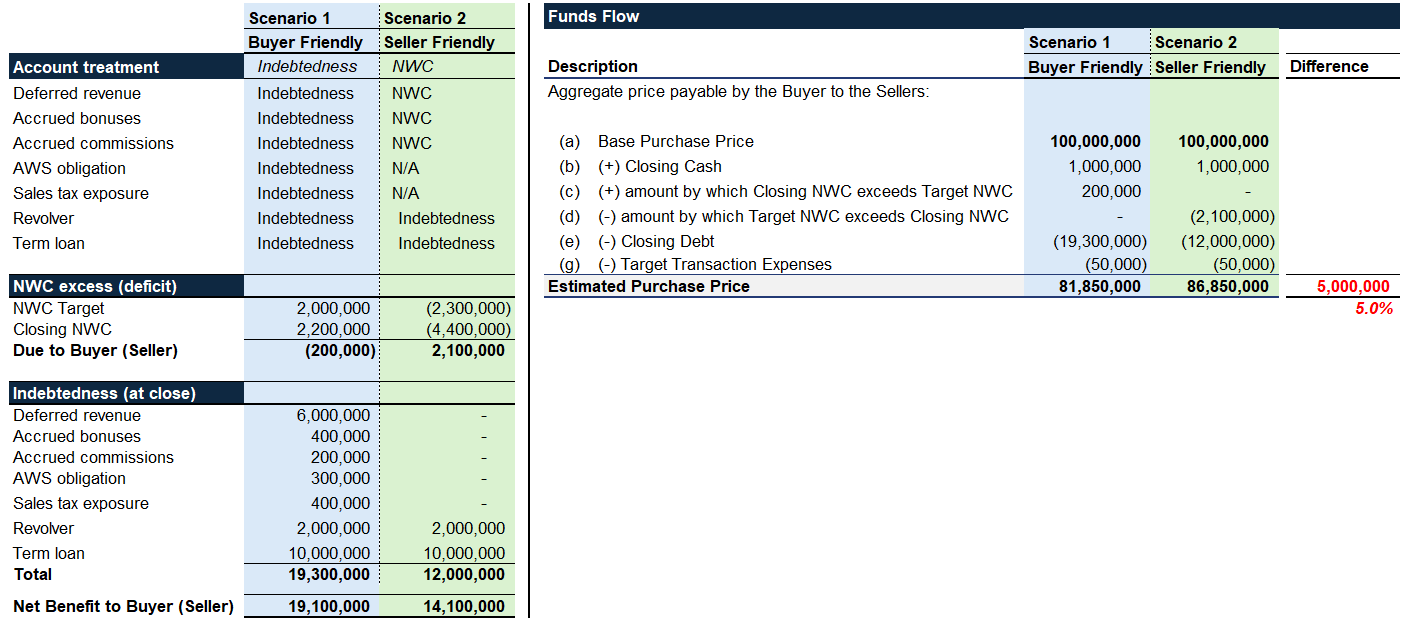

The Real Difference: Example Funds Flow

The impact on deal value can be demonstrated using the example below:

Scenario 1

In both scenarios, the revolver and term loan were classified as debt. In Scenario 1, however, a $300,000 AWS commitment and a $400,000 sales tax exposure were identified during diligence and are treated as debt-like items (despite not appearing on the balance sheet).

In addition, the buyer has negotiated for deferred revenue, accrued bonuses, and accrued commissions to be stripped out of NWC and classified as indebtedness.

Scenario 2

In Scenario 2, the AWS commitment was considered normal course (and excluded from debt), the sales tax exposure was not quantified, and deferred revenue, accrued bonuses, and accrued bonuses were considered normal course NWC liabilities.

The bottom line

All else being equal, one might expect these classification differences to have a minor, if not immaterial, impact on total deal value. However, what might otherwise seem like small tweaks to the purchase agreement on a $100 million deal results in a purchase price reduction of approximately $5 million, or 5%.

Accordingly, the negotiation of how to define indebtedness and NWC and the resulting treatment of these items should be a top priority for all parties.

Practical Considerations for Buyers and Sellers

For buyers, the priority should be to anchor purchase agreement definitions based on cash flow impact rather than traditional accounting classification. This includes considering the cost and effort required to service deferred revenue, identifying and diligencing all off-balance sheet commitments, and ensuring that all material future cash obligations are appropriately captured.

Sellers should be prepared to clearly articulate why key items (e.g., deferred revenue, commissions and bonuses) are operational in nature and should not be treated as indebtedness. Supporting analyses around tax exposures and accrual methodologies can help avoid late-stage surprises.

For both parties, clearly outlining working capital and indebtedness expectations in the LOI is ideal, but negotiating throughout the deal process (and not waiting until the purchase agreement is being drafted) is critical. The parties that approach these purchase agreement definitions with precision are best positioned to preserve value and avoid post-close disputes.