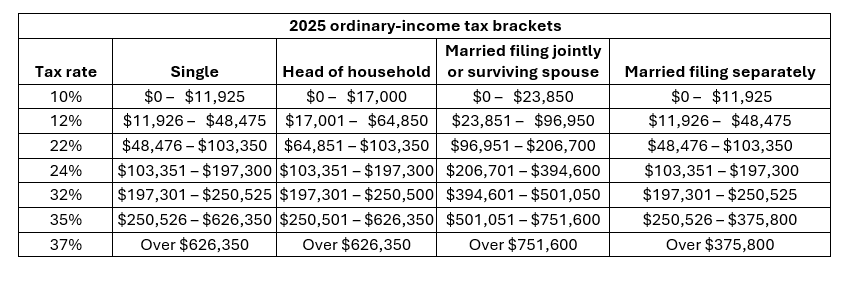

The conventional tax wisdom is typically to accelerate tax deductions into the current year and defer taxable income until the next year, assuming you won’t be in a higher tax bracket next year. If you’ll likely be in a higher tax bracket in the near future, you may want to flip this strategy.

In recent years, this strategy has also been impacted by the possibility of increased tax rates. This is less of a consideration with the passage of the OBBBA, since the more favorable tax rates and brackets of the TCJA, which were otherwise set to expire after 2025, have been made permanent.

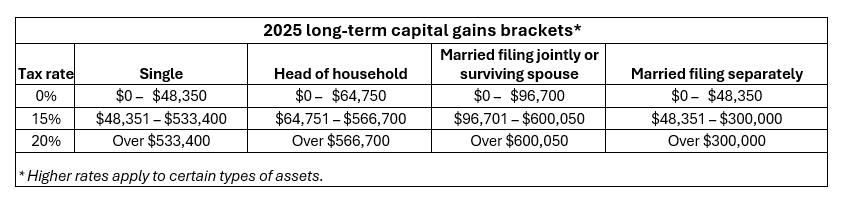

Long-term capital gains rate

The long-term capital gains rate applies to realized gains on investments held more than 12 months. For most types of assets, the rate is 0%, 15% or 20%, depending on your income level. In addition, the 3.8% Net Investment Income (NII) tax applies for taxpayers over certain income levels. See more on the NII tax in our Tax Planning For Investors.

Itemized Deductions

The TCJA suspended several itemized deductions for 2018 through 2025 while boosting the standard deduction. The OBBBA generally made these changes permanent with some modifications.

Tip: The standard deduction for 2025 is generally $15,750 for single filers and $31,500 for joint filers and will be $16,100 and $32,200, respectively, in 2026. An additional amount is added for those 65 and older, ranging from $1,600 to $2,000 per person depending on filing status. In addition, beginning in 2025, a new “bonus” deduction of $6,000 per eligible individual ($12,000 for married couples) is available for those aged 65 and older, subject to a modified adjusted gross income (MAGI) phase-out threshold. This bonus deduction is available even for taxpayers who itemize deductions.

Beginning in 2026, the OBBBA includes a return to a high-income limitation on itemized deductions in the form of a new 2/37 (5.4%) reduction in itemized deductions that would otherwise be allowable for taxpayers to the extent they have income subject to the 37 percent tax bracket.

YEAR-END MOVE: If you expect to itemize deductions on your 2025 tax return, take advantage of several key deductions that can lower your tax bill. Consider the following:

- Donate cash or property to a qualified charitable organization (see more below).

- Pay deductible mortgage interest if it makes sense for your situation. This includes interest on acquisition debt up to $750,000 for your principal residence and one other home.

- Make state and local tax (SALT) payments up to the annual deduction limit. Under the OBBBA, the SALT cap is quadrupled from $10,000 to $40,000 for 2025. The cap then increases by 1% annually through 2029 before reverting to $10,000 in 2030. This increase in the SALT cap is phased out for taxpayers with MAGI between $500,000 and $600,000 so that the lower $10,000 cap still applies at income levels above $600,000 (lower thresholds apply for married taxpayers filing separately).

- Do home improvements that qualify for mortgage interest deductions as acquisition debt. This includes loans made to substantially improve a qualified residence.

- Schedule non-emergency physician or dentist visits like exams or cleanings in 2025 if you expect to qualify for a medical deduction this year. Only unreimbursed expenses above 7.5% of your adjusted gross income (AGI) are deductible.

Tip: Conversely, if you do not expect to qualify for a medical deduction in 2025, absent other circumstances, you might as well delay non-emergency expenses to 2026 when they might do you some tax good.

Charitable Donations

The tax law allows you to deduct charitable donations within generous limits if you meet certain recordkeeping requirements, but the OBBBA adds several tax complications.

YEAR-END MOVE: Bunch charitable donations in a year in which you expect to itemize. For instance, if you are itemizing in 2025, you may step up charitable gift-giving before January 1st. As long as you make a donation this year, it is deductible in 2025 – even if you charge it on a credit card.

- For the first time ever, the OBBBA imposes a floor of 0.5% of AGI before you can claim any charitable deduction, beginning in 2026. Also, charitable contributions will be included in the itemized deduction phaseout starting in 2026 for taxpayers in the 37 percent income tax bracket, as discussed above.

- These new limitations may be especially important if you are planning to donate appreciated long-term gain property that would qualify for a deduction equal to the property’s fair market value (FMV). The deduction for property is limited to 30% of AGI, whereas monetary contributions are limited to 60% of your AGI. If giving a combination of property and cash, the 30% limitation continues to apply along with an overall contribution limitation of 50% instead of the 60% limitation available where only monetary contributions are made. Any excess above these thresholds may be carried over for up to five years.

- Donor Advised Funds (DAFs) may be an excellent vehicle for taxpayers desiring to “bunch” their itemized deductions or donate appreciated securities or other noncash assets in 2025, particularly if they are also seeking to obtain a charitable contribution deduction this year while deferring payment to the ultimate charitable beneficiary until a later date. Consult your tax or investment advisor for more details.

- Qualified Charitable Distributions (QCDs): Individuals aged 70 ½ or older can make QCDs of up to $108,000 directly from their IRA to qualified charities, which is not impacted by the new deduction limits and is excluded from taxable income.

Tip: Beginning in 2026, the OBBBA also allows a charitable contribution deduction of up to $1,000 for non-itemizers. The maximum deduction is doubled to $2,000 on a joint return.

Home Energy Credits

If you own your principal residence, you may benefit from two types of “home energy” tax credits on your 2025 return.

YEAR-END MOVE: Make energy-saving installations before the end of the year to secure credits for qualified improvements. Under the OBBBA, both credits will expire after 2025 and are not expected to be renewed.

The two credits still available before 2026 are as follows:

- Energy Efficiency Home Improvement Credit: This is a 30% credit for qualified expenses like insulation, central air conditioners, water heaters, furnaces, heat pumps, biomass stoves and boilers and home energy audits, with varying dollar caps on the credit amount depending on the type of expenditure.

- Residential Clean Energy Credit: This is a 30% credit for the cost of new qualified clean energy property like solar electric panels, solar water heaters, wind turbines, geothermal heat pumps, fuel cells and battery storage technology.

Tip: Other special rules and limits may apply to certain qualified expenses. Obtain confirmation of tax breaks before making any commitments.

Alternative Minimum Tax

The alternative minimum tax (AMT) calculation features technical adjustments, inclusion of “tax preference items” and subtraction of an exemption amount, subject to a phase-out. After comparing AMT liability to regular tax liability, you effectively pay the higher of the two.

YEAR-END MOVE: Have your tax professional assess your AMT status. When it makes sense, you may shift certain income items to 2026 to reduce AMT liability for 2025. For instance, you might postpone the exercise of incentive stock options (ISOs) that count as tax preference items.

Due to changes in the TCJA and other legislative modifications, the exemption amounts for the AMT have increased steadily in recent years, as shown below.

The OBBBA permanently establishes an exemption phase-out threshold of $500,000 for single filers and $1 million for joint filers, with inflation indexing, beginning in 2026 (reverting the threshold to the 2018 amount), and the new law also doubles the rate for phasing out exemptions. So, for 2026 and beyond, AMT exemptions for higher-income taxpayers will be phased out faster which means more taxpayers may owe AMT.

Tip: The AMT has only two tax rates: 26% and 28%. If you are sure that you will have to pay the AMT in 2025 and your top AMT rate is lower than your top regular rate, for example the highest rate of 37%, you might accelerate income into 2025.

Family Tax Breaks

If you are a parent with young children, you may be entitled to several tax breaks designed to reduce your family’s tax burden.

YEAR-END MOVE: Maximize the tax benefits for your situation. This may comprise one or more of the following tax provisions generally enhanced by the OBBBA.

- For 2025, parents may claim a Child Tax Credit (CTC) of $2,200 for each qualifying child, subject to a phase-out beginning at $200,000 for single filers and $400,000 for joint filers.

- The dependent care credit is enhanced for certain taxpayers with a modified adjusted gross income (MAGI) below specified levels. For high-income taxpayers, the maximum credit remains $600 for one child and $1,200 for two or more children.

- Previously, the adoption credit was 100% non-refundable. Beginning in 2025, the new law provides that up to $5,000 of the credit is refundable, indexed for inflation in the future.

- Under the TCJA, parents could withdraw up to $10,000 tax-free from a Section 529 plan for higher education to pay a child’s tuition at a qualified elementary or secondary school. The OBBBA doubles the cap to $20,000, beginning in 2026.

Tip: The maximum annual amount that can be contributed to a flexible spending account (FSA) for dependent care expenses increases from $5,000 to $7,500, beginning in 2026.

Miscellaneous

- The OBBBA introduced a deduction of up to $10,000 for interest paid on an automobile loan in 2025-2028 for a qualified new vehicle purchased after 2024. The deduction is available for both itemizers and non-itemizers but phases out for taxpayers with MAGI over $100,000 ($200,000 for joint filers) and additional restrictions apply.

- Pay tuition in 2025 for a child’s semester beginning in early 2026 if you can claim one of two higher education credits. However, both credits are subject to phase-outs based on MAGI.

- Avoid an estimated tax penalty with a safe-harbor exception. Generally, a penalty will not be imposed if you pay 90% of your current year’s tax liability or 100% of your prior year’s tax liability (110% if your AGI exceeded $150,000).

- Empty out FSAs for health care or dependent care expenses if you will forfeit unused funds under the “use-it-or-lose it” rule. However, your employer’s plan may provide a carryover to 2026 of up to $660 of unused funds or a 2½-month grace period.

- If you own property damaged in a federal disaster area in 2025, you may elect to obtain fast tax relief by filing an amended 2024 return. The TCJA suspended the deduction for casualty losses for 2018 through 2025 but retained a current deduction for federal disaster-area losses. The OBBBA extends this tax break and allows deductions for losses in state-declared disaster areas, beginning in 2026.

We Are Here to Help

A well-planned approach can reduce your tax burden and create greater financial certainty heading into the new year. Whether you are evaluating charitable contributions, exploring energy credits, or preparing for changes to itemized deductions, we are here to guide you. For more year-end insights, explore our related articles, including 2025 Year-End Tax Planning for Business Owners and 2025 Year-End Tax Planning for Investors and Estate & Gift Planning. Contact us today if you have questions about these updates.